SBTi v2.0: New Rules for Corporate Net Zero and Carbon Credit use

Reading Time: 4min

The Science Based Targets initiative (SBTi) published Version 2.0 of its Corporate Net-Zero Standard on June 11, 2026, marking a turning point for global climate target setting. More than 13,600 companies align their climate goals to SBTi and 2,622 of them use the specific Net-Zero framework (as of June 2026). The new standard version officially integrates carbon credits and permanent carbon removal as essential components for achieving net-zero.

Summary

SBTi v2.0 officially integrates carbon credits especially durable carbon removal into the standard.

Permanent Carbon Removals for residual emissions become mandatory for large companies starting in 2035

A voluntary recognition programme rewards early action from 2027

A "like-for-like" durability rule directs capital toward long-lasting removals

Taking Ownership for Emission Responsibility

The headline change is the OER framework, which replaces the older, vaguer Beyond Value Chain Mitigation (BVCM) guidance. It's the first time SBTi has created a structured route for carbon credits in corporate net-zero strategy. With this approach, companies are incentivized to take voluntary action already before 2035 and will be recognized for their action with different “labels”:

Engaged: address at least 1% of ongoing Scope 1–3 emissions, via tonne-for-tonne credits.

Advanced: cover 100% of Scope 1–2 plus enough Scope 3 to reach ~10% of total ongoing emissions, at a $20/tCO₂e carbon price or via tonne-for-tonne credits.

Leadership: apply an $80/tCO₂e contribution budget to 100% of ongoing emissions, with any surplus funding further climate action.

Concretely, SBTi will maintain a Dashboard with the climate contributions levels of companies.

Crucially, OER is not a loophole. Credits do not count toward Scope 1, 2, or 3 reduction targets - these remain visible and tracked separately. Companies must still cut their own emissions as a main priority.

OER addresses the "ongoing emissions" that remain during the transition.

V2.0 also splits companies into two categories (A and B) by size and geography. Category A (large companies globally, plus medium-sized firms in high-income countries) faces the strictest requirements, including the mandatory 2035 removal obligation.

Carrot before stick - obligation from 2035

From 2035, large (Category A) companies must buy carbon removals, starting at 1% of their footprint and rising each year linearly to 100% at their net-zero date.

“By their net-zero target year and thereafter, all companies with net-zero targets are expected to reduce emissions to zero or residual levels and neutralize 100% of residual emissions using eligible carbon removals, either directly or jointly with value chain partners.” - SBTI

What Carbon Credits can be used?

Verified Mitigation Outcomes & Carbon Removals

SBTi allows the use of Verified Mitigation Outcomes (VMO) which is the broader category of ex-post, climate result delivered by the use (called "retirement") of a carbon credit.

Outcomes must be measured after the fact, independently verified, and can include both reduction/avoidance and removal credits.

Any VMO can be used under the OER framework. After 2035, the standard narrows to the use of removals only, so avoidance credits have no role there.

Like-for-like principle

An important classification SBTi makes is the "like-for-like" principles: long-lived residual emissions of a company will have to be neutralized with long-lived removals specifically - for example 1000+ year biochar carbon removal credit.

High-quality Carbon Credits

Companies must ensure every supported activity meets recognized third-party high-integrity criteria: documented due diligence, do-no-harm safeguards, avoidance of carbon lock-in, and annual transparency. The SBTi will develop criteria and processes for recognizing third-party frameworks, standards, and programs, where applicable.

How early are we, really?

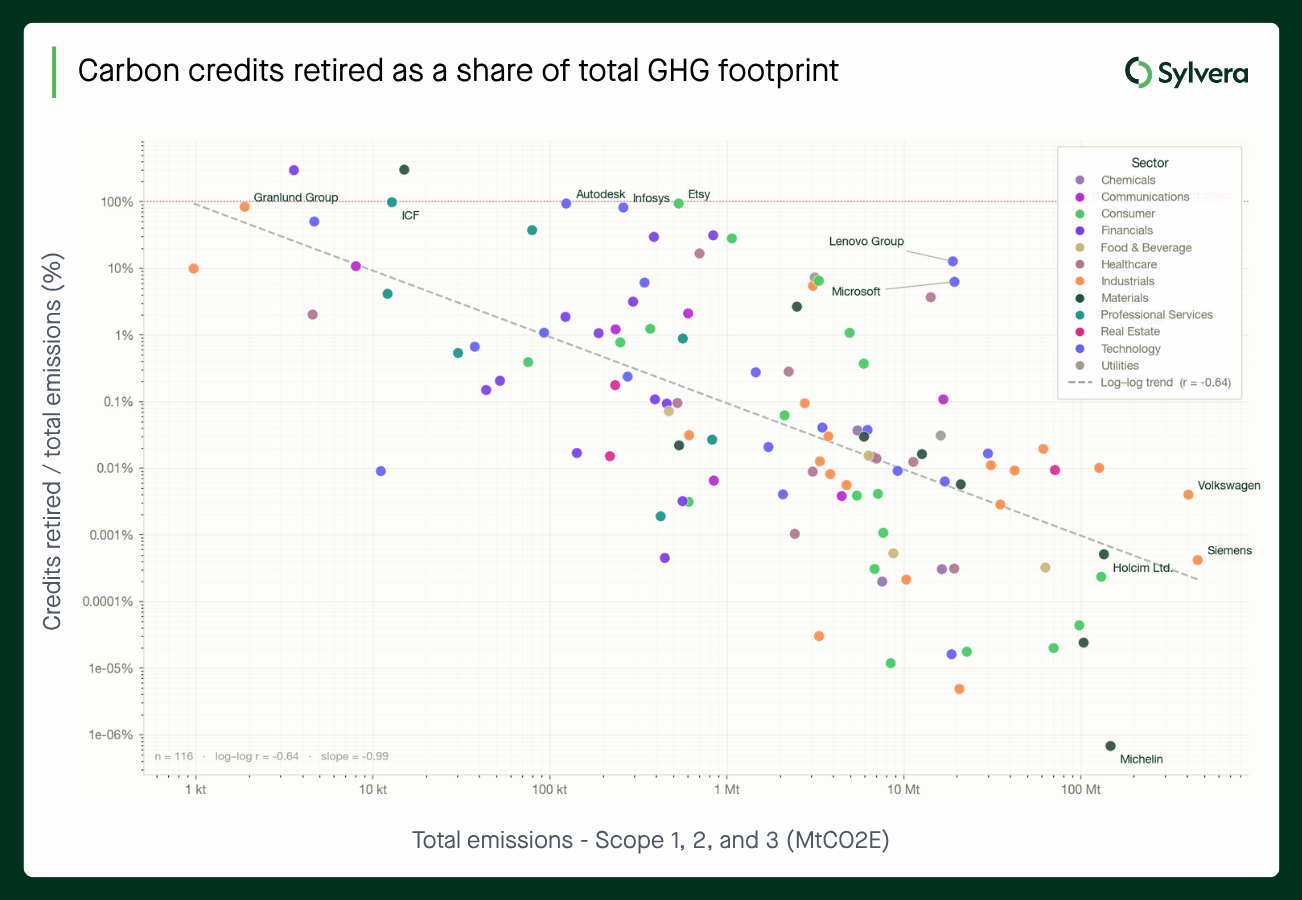

New data from SBTi and Sylvera shows just how early-stage corporate carbon credit demand is. Companies with SBTi validated targets - roughly 11,000 globally in 2025, covering an estimated 34 billion tCO2e across Scopes 1-3 - retired around 20 million tonnes of credits. That's just 0.06% of their total emissions.

The following chart from Sylvera shows the % of emissions covered by carbon credit used (vertical axis) versus the total volume of tonnes of CO2 compensated (in Million tonnes or “Mt”).

Carbon credits retired as a share of total GHG Footprint. (Source: Sylvera)

Carbon credits retired as a share of total GHG Footprint. (Source: Sylvera)

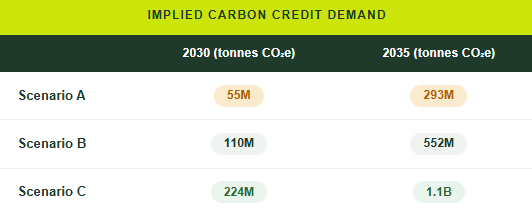

Sylvera forecasts demand could climb toward ~293 million credits by 2035 under certain scenarios if companies follow the new rules.

Total credit demand pre-2035 from SBTi-aligned companies. (Source: Sylvera)

Total credit demand pre-2035 from SBTi-aligned companies. (Source: Sylvera)

From 20 million tonnes today, that's a step-change - and it rewards quality and permanence, exactly where credible removals win.

Beyond Credits: Additional Changes

Further important innovations in Version 2.0 include:

Energy Attribute Certificates (EACs)

Companies can use certificates (like renewable energy credits) to back up their climate claims, but these are kept separate from their actual measured emissions so the two don't get mixed up.

EAC from low carbon steel, ammonia, biofuels such as Sustainable Aviation Fuels can also be used as Scope 3 indirect mitigation tool to address indirect supply chain emission for example in logistics and transport, specifically for emissions that cannot yet be directly addressed due to infrastructure or supply constraints

Mandatory transition plans

Larger companies must publish a detailed roadmap showing exactly how they intend to reach net-zero.

Best-effort basis

A company that takes genuine, credible action can still be considered compliant even if it just misses its target.

Duty to explain

If a company chooses not to take responsibility for its ongoing emissions, it has to say so publicly and explain why.

Implications for Planet2050

As carbon credits move from optional gesture to regulated obligation, the question shifts from "Should we do this?" to "How do we reliably remove CO2 at scale, with assets that are trusted, financeable, and custody-eligible?"

SBTi v2.0 rewards exactly the high-quality climate outcomes and carbon removals for which Planet2050 is building the architecture.

The time before 2035 is a strategic window. Investors who secure offtake now are positioned for the mandatory phase; hesitation carries the risk of acute supply shortages.

Note: This article reflects Planet2050's interpretation of the SBTi Corporate Net-Zero Standard v2.0 as published in June 2026. Thresholds, timelines, and demand forecasts derive from the standard and third-party analyses; companies should consult the official standard for compliance decisions.

_____

Stay ahead of the market

Go to the SBTi Corporate Net-Zero v2 page

Investor Updates: Sign up on our Investor Page to stay informed on our upcoming listing.